FinancialData is basically a wrapper for Yahoo Finance's API and a couple of others. It's possible this might be caused by some issue with their API.

Instead of

FinancialData["GE", {2011, 1, 1}]

try evaluating:

Import["http://ichart.finance.yahoo.com/table.csv?s=GE&a=0&b=1&c=2011&d=9&e=12&f=2014&g=d"]

Does this work? If not, then Yahoo's Finance API is down for some reason.

There are other ways of getting financial data into Mathematica. One is via the WolframAlpha function:

http://support.wolfram.com/kb/7357

Or you can use the EntityFramework. Hit "Ctrl + = " and type something like "GE closing prices since 2011"

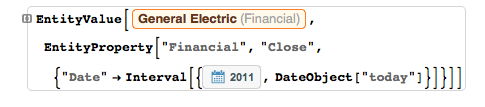

It shows you what code you'd use for this task:

In copyable code that's:

EntityValue[Entity["Financial", "NYSE:GE"], EntityProperty["Financial", "Close", {"Date" -> Interval[{DateObject[{2011}], DateObject["today"]}]}]]