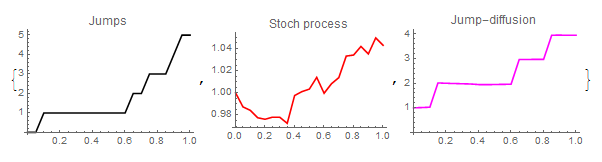

Jump diffusions play important part in the theory of random processes where the underlying variable is affected by additional source of randomness. Jumps have been added to the repository of tools and methods in quantitative finance to help explaining spikes and shocks to the data in equity, credit or commodity markets. We explore this subject with the help of Mathematica 10 which provides excellent toolkit to handle jump diffusions in arbitrary setting.

Attachments:

Attachments: