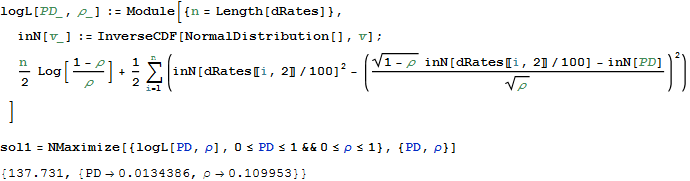

2 simple ways to perform (simple) Maximum Likelihood Estimation in Mathematica:

(1) Construct the Log-Likelihood function and maximize it:

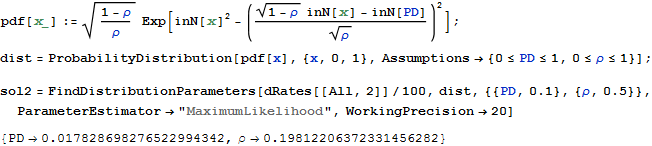

(2) Define the Probability Distribution and find parameters:

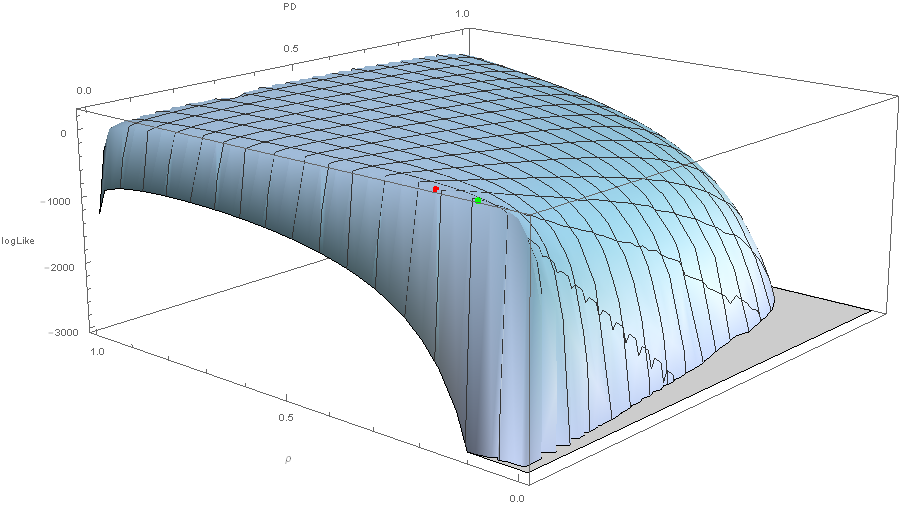

They are not that much different, in the sense that they yield close values for the Log-Likelihood function (shown in the plot below), but still, the difference is noticeable in the resulting values of the parameters and I am curious which should I trust more?

Attachments:

Attachments: