Hi Igor,

I have tried to replicate your results related to the cumulants and the gaussian filter but I haven't been able to get the same results as you. All the previous calculations were ok.

Here's my code and the resulting graphs:

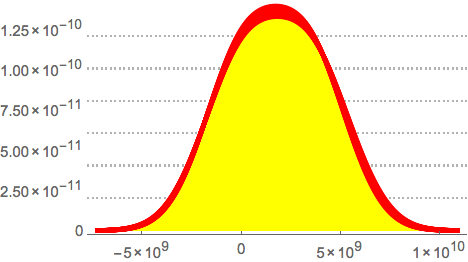

cs = TimeSeriesAggregate[jpyhdata, "Quarter", Cumulant[#, 2] &];

SmoothHistogram[cs, PlotTheme -> "Business", PlotStyle -> Red,

Filling -> Axis, FillingStyle -> Yellow]

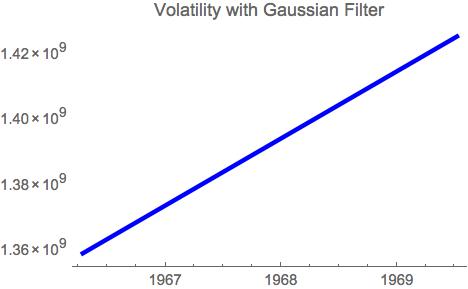

DateListPlot[GaussianFilter[hvol, 4], PlotTheme -> "Web",

PlotStyle -> Blue, PlotLabel -> "Volatility with Gaussian Filter"]

May I know what I'm doing incorrectly?

Many thanks in advance,

Ruben