Hi Anton,

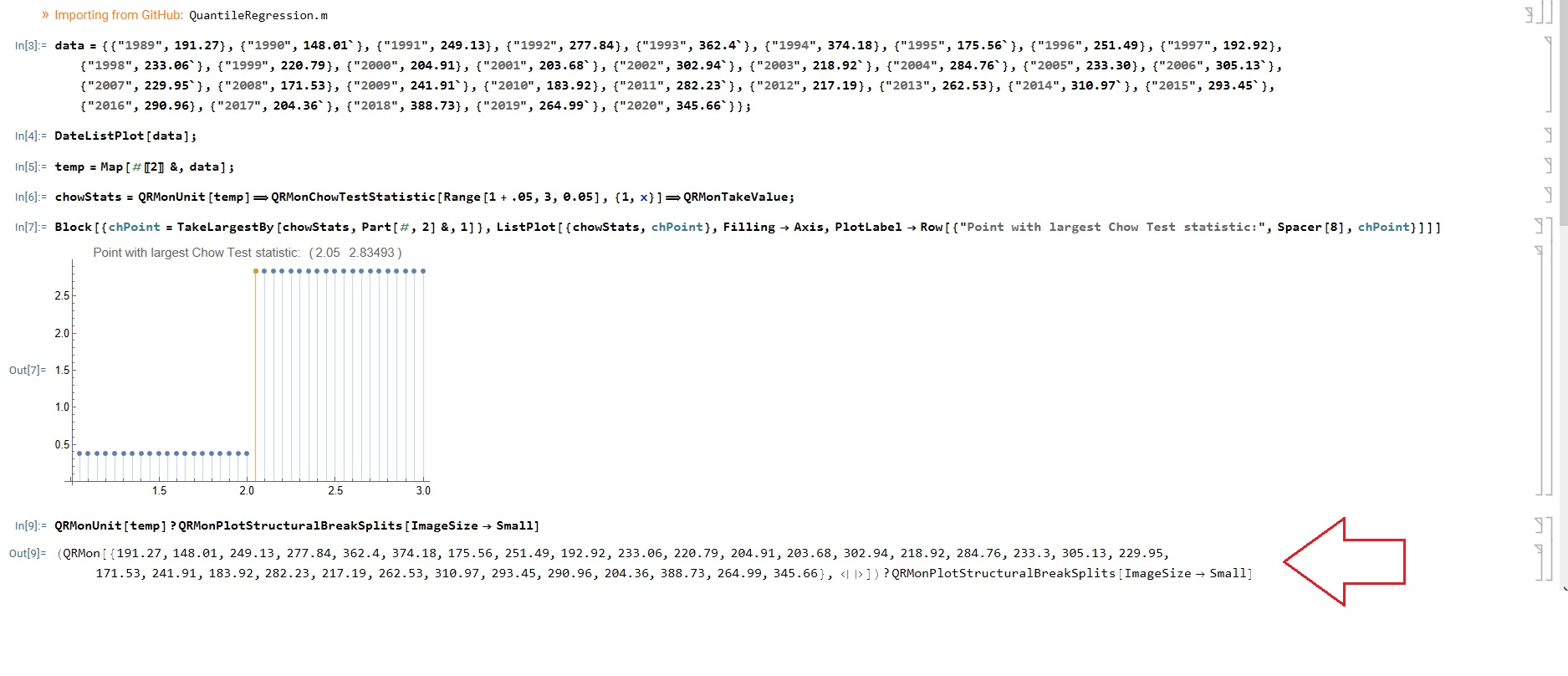

Thank you for sharing the excellent package. How do I determine the year of the breaking point? I am a beginner in Mathematica. sorry.

data = {{"1989", 191.27}, {"1990", 148.01`}, {"1991",

249.13}, {"1992", 277.84}, {"1993", 362.4`}, {"1994",

374.18}, {"1995", 175.56`}, {"1996", 251.49}, {"1997",

192.92}, {"1998", 233.06`}, {"1999", 220.79}, {"2000",

204.91}, {"2001", 203.68`}, {"2002", 302.94`}, {"2003",

218.92`}, {"2004", 284.76`}, {"2005", 233.30}, {"2006",

305.13`}, {"2007", 229.95`}, {"2008", 171.53}, {"2009",

241.91`}, {"2010", 183.92}, {"2011", 282.23`}, {"2012",

217.19}, {"2013", 262.53}, {"2014", 310.97`}, {"2015",

293.45`}, {"2016", 290.96}, {"2017", 204.36`}, {"2018",

388.73}, {"2019", 264.99`}, {"2020", 345.66`}}