I see your point. On the other hand the problem that you encountered is mostly because the time series is to equidistantly sampled, because there are no data points on the weekends. So getting the data is rather straight forward, but the sampling needs to be taken into consideration. I think that that's more of a data analysis problem, rather than a curated data problem.

To fix the sampling issue I separated the "data from the dates" , then did the forecast bit, and then added the dates in again. You could use several alternative strategies, e.g. use the Function TimeSeriesResample you can also fix the problem; and I only have to work with TimeSeries data. The idea is like this:

dkfresamp = TimeSeriesResample[dkf];

I then fit a model (which in this case is not a good one!):

model = EstimatedProcess[dkfresamp, ARIMAProcess[{a, b, c}, d, {e, f}, g]]

I then forecast

forecast2 = TimeSeriesForecast[model, dkfresamp, {20}, Method -> "Kalman"]

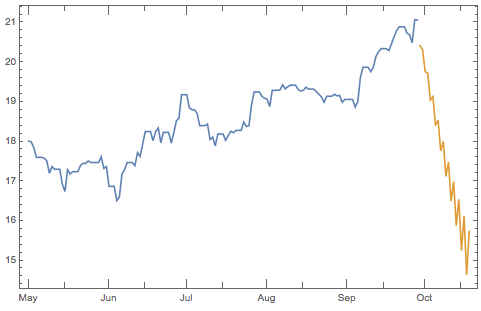

and plot:

DateListPlot[{dkfresamp, forecast2}]

Of course the fit is quite unsatisfactory in this case, but the program runs through without any error messages and I do not need to split the dates from the values.

Best wishes,

M.

PS: If you want the time series in a standard date, value format you can use:

dkfresamp2 = {DateList[#[[1]]], #[[2]]} & /@ dkfresamp;